#3 Universal Laws of Insurance Planning

#3 Universal Laws of Insurance Planning

Using statistics to buy critical illness insurance in a cost-effective way

Hello readers,

I chanced upon this article on Critical Illness Statistics in Singapore, here is my analysis on it. As this article is rather technical and lengthy, I’d advise that you pull up your portfolio so you can run through the checklist and ensure that you are adequately covered. Hope this helps to simplify the research you have done!

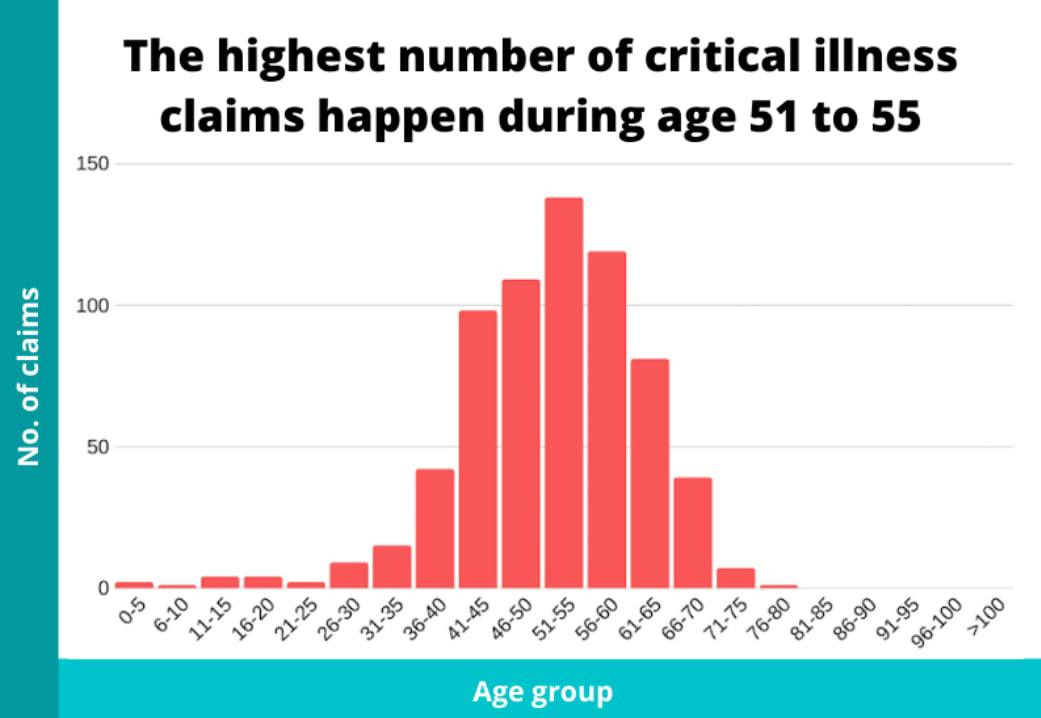

Critical Illness statistics resembles... a normal distribution?

The first chart shows the statistical probability of contracting a critical illness for each age group, with the highest claim rates occurring in the age ranges of 26-75.

The second graph depicts a normally distributed curve.

We can see that the higher probability areas are highlighted in pink and purple while the lower probability areas are highlighted in green.

This is very similar to the first chart whereby the probability of contracting a CI high from age 26-75, and low before age 26, and after age 75.

Thus we can reasonably conclude that the probability of critical illness claims resembles a normal distribution chart.

So does this mean that we only buy critical illness insurance when we turn 26?

Let's draw a parallel with a relatable example, the S&P500 stock market index!

It generally follows a normal distribution as well with an ‘average’ return of 10% per year. (pink and purple portion)

Outlier events such as:

The GFC caused the market to drop by 58%

COVID saw it drop by 35% (green portion on the left)

Post-COVID, the market shot up by more than 100% (green portion on the right).

Although the probability is small, if a large market capitulation does happen, the impact on the portfolio would be massive.

For example, if your portfolio is down 50%, you will need to double your portfolio to get back to breakeven which is either very tough or takes a long time.

We can apply this same concept back to Critical Illness insurance.

If we choose not to buy before age 26, the low probability of occurrence may mean that we are temporarily 'wasting money', but the impact is huge if we do contract one, i.e:

Bad case - The premium you pay is increased by a certain percentage

Worse case - You are excluded for the medical condition you contracted

I.e if one suffers from a slipped disc, he/she may be excluded for spine-related conditions. If one suffers from asthma, respiratory conditions will be excluded. And the chances of reoccurrence of a critical illness are high in the initial years hence you may not have funds if you contract it a second time.

Worst case - The company denies you from even buying insurance aka you aren’t covered for ANY illness.

What's the best solution then?

• The most cost-effective way would be to stack majority of your CI insurance 'position' with temporary term insurance every few years to solve the problem on the left and middle. (before age 75)

• The green portion on the right can be solved with either permanent whole life critical illness insurance, or term insurance till your expected life expectancy age (for males ~age 90, for females ~age 95-100)

With that being said, here is an insurance planning checklist you can follow.

10 Universal Laws of Insurance Planning (Singapore context)

Hospital insurance is a no-brainer, you are paying a known premium instead of an unknown hospital bill. Also, you will not able to access majority your Medisave funds for your whole life, might as well use it to buy the best plan.

For accident insurance, focus on the medical expense reimbursement coverage (i.e covering MRI, physiotherapy and TCM treatment)

If you are single, buy ONLY term insurance. ((However if you wish to make any charitable donations to family members or organisations, feel free to buy whole life insurance.)

If you have a family, ask yourself if you wish to leave them a sum of money after your death. If the answer is no, buy term insurance. If the answer is yes, buy term insurance till your expected life expectancy, or universal whole life insurance depending on your cashflow.

Buy critical illness term insurance till age 75.

Only buy whole life critical illness insurance if you want to have access to alternative medical treatment after age 75.

Purchase disability income insurance to cover conditions NOT covered by your life insurance policy.

Make sure your insurance costs 10-15% of your monthly income MAX.

With your extra monthly cash surplus, save cash, pay down debt or invest in assets you UNDERSTAND (be it a business, property, etc)

Check if your agent has skin in the game. If they do not have the same products they recommend you, do not hesitate to end the conversation.

For Law #6, alternative medical treatment costs anywhere between $500,000 to $1 million in today’s value. For a rough estimation of the cost during your retirement years, compound the numbers with an appropriate inflation rate.

Insurance is a COST, you should be thinking of the least amount of dollar outlay for maximum coverage.

One needs to take into account the decline in human capital value as one ages.

Lastly, if you trust your agent and he/she checks the last criteria, do not hesitate to buy the solutions. You will likely never feel the need to buy life insurance until an injury or sickness strikes you. And by then, it’ll probably be too late. (Coming from someone who’s suffered from a slipped disc and two wrist injuries, my future insurances will probably exclude these conditions)

If you want a free no-BS review of your portfolio, drop me a dm. Cheers ✌️